Friday, December 31, 2021

Key similarities and differences between central banks and financial & banking institutions

Banks play a key role in the financial sector by contributing to economic growth and the services of individuals and entities. In addition to the basic function of lending, banks can provide various other services that help the economy to function smoothly. Serving the general public with a variety of services, they perform representation functions such as collecting bills of exchange, offering pension and insurance services with the aim of social responsibility, pushing for savings and protection (compensation for property and accidents). But by offering investment products, acting as financial advisers helping their clients with stock quotes, bond offers as well as mergers or acquisitions.

In contrast, the central bank is a financial institution where it differs from the rest. It is the body that regulates the entire banking and monetary system of the country, finding the ways by which it will achieve the goals set by the government (inflation targets) in order to maintain economic stability, managing the monetary and credit system of the nation. It is a non-profit public institution unlike the rest where it can be either public or private with non-profit functions. The link between the two is the role of the central bank to regulate various parameters of commercial banks such as the ratio of cash reserves, the legal liquidity ratio and also exercising direct controls in cases of ethics and emergency lending of banks.

Tuesday, December 7, 2021

The opportunities for a bank to enter foreign markets.

There is a wide range of theories in the explanation behind the logic of bank expansion abroad, which provides possibilities that vary from case to case. Depending on how a bank chooses to enter a foreign market, it acquires the corresponding exposure in it. The simplest form of entry is through correspondent banking where you do not need a physical presence abroad, acquiring basic cash management services, transactions (domestic, foreign currency) and trade credit. It can be argued that responsive banking is not a strategy of competitive entry into foreign markets but an offer of services in foreign financial markets and to serve international customers without having to open branches abroad. Banking services for credit facilities (loans, overdrafts and pending loans) are not easily provided without the Bank's representation in the market.

When deciding to enter they should consider the cost of entry, exit and operation. The way to bring the lowest possible cost is a representative office, where it can not operate independently but only to attract and create business activities for the parent bank. Entry methods are different for different types of banks, specialized banks such as investment banks aαre more attractive in getting representative offices than setting up an agency or branch as there is no need to access basic functions such as deposits and loans but mainly financing the holding of securities through the commitment of these securities in repurchase agreements (repo). The branch in the foreign market is not an independent legal entity but an integral part as a legal and operational part of the parent company. The decision-making process is not fully outsourced but has greater autonomy compared to domestic branches, providing all the functions allowed by the host country's banking authorities where they are subject to banking supervision by both the parent company and the branch. . If it wants to enter as a separate legal entity to have its own funds, it will choose the subsidiary where it can be the result of an acquisition or a newly established company (greenfield) signaling a greater commitment with a more positive assessment of prospects for sustainability and business efficiency.

The financial operation of the bank that has entered the foreign market in addition to the functions of secured financing with assets, discounting invoices and agency. It has to do with the size of the foreign market client where traditional bank loans and overdraft financing are for relatively small businesses with international operations, as opposed to multinational bonds and syndicated loans. In general, the possibilities offered by a bank in financing bonds and letters of credit to foreign companies can be differentiated based on the company's experience in the market, issuing European Shares and Letters of Credit (LOC) for start-ups and securities, fund management, guarantees, collateral, and syndicated loans to finance essential projects.

Wednesday, December 1, 2021

Why the Central Banks should be independent?

The central bank's crucial role is to ensure the stability of the currency through complete independence while keeping inflation levels low and stable. But it is not often where its role will lead to preventive oversight of functions that are inextricably linked to action. For example, the functions of a central bank tax representative. In addition, the financial sector of the central bank with regulatory functions and advisory powers, as well as its own participation in the financial system allow to encourage the development of the sector, which will require close coordination with the government, for example in legal reform.

Economists argue that banning monetary financing of governments is a key element in ensuring the operational independence of a central bank. By protecting its independence, it helps ensure that monetary policy decisions are geared towards monetary objectives while maintaining the health of the economy, rather than having to accept pressure from public authorities to help finance government deficits. But it is very common for a central bank to declare independence of an institution without independence of purpose. In this case, the government sets its own monetary policy goals and leaves the choice of instruments to the central bank, depriving it of long-term economic stability.

Tuesday, November 30, 2021

The growing use of cryptocurrencies and the affect in banking system, financial markets, equities and monetary policy?

The first cryptocurrency appeared in 2009 in decentralized markets. They are not issued or endorsed by a central authority such as a government or a monetary financial institution. Acquisition can be done through the mining process in order to confirm the pending transactions. However, cryptocurrencies can be bought and sold through exchanges and stored electronically. The increase in exchange volume shows that it is now accepted, with famous banking systems changing and adapting to the rapid developments considering adopting a blockchain system similar to cryptocurrencies where peer-to-peer technology and decentralized system have the ability to upgrade the role of banks in the modern financial infrastructure. There is a favorable attitude towards the adoption of cryptocurrencies but also the investment by financial institutions in them.

The idea of easy money and the growing volume of transactions with the constant fluctuations of prices in its short life cycle, not knowing the instability and the risk created many upheavals that hindered the wide acceptance as a means of investing and saving in the financial markets. The attempt to stabilize the price of currencies has led to fixed currencies where they can be pegged to a currency such as the dollar or to the price of a commodity such as gold having linked their market value to external factors and through algorithmic buying and selling mechanisms is restored. part of the short-term instability.

The main reason for the creation of cryptocurrencies is due to the use of encrypted transactions that guarantee some anonymity and transparency through the chain of blocks, thus reducing transaction costs as no intermediary is involved. Despite the advantages, the loss and exposure to digital risks is an important factor and in combination with the initial growth where it is located, raises many doubts in the universal use as a public through monetary exchange as it should maintain its purchasing power while keeping inflation as low as possible. , sufficient to encourage spending instead of storage.

The decentralized cryptocurrency system based on technology without an intermediary has the potential to replace a banking system in which a monetary policy is responsible for decisions that affect the economic fortunes of countries. An example is the financial crisis of 2008 where central banks had a negative impact on consumers and the economy as they were responsible for the debilitating recession. However, it suffers from multiple disadvantages including limited supply as it is a product of e-mining and the lack of legal status in most economies. Following technology, central banks are in the process of developing their own digital currency in order to remove intermediaries, thus reducing transaction fees, such as retail banks, and will use encryption to ensure that it is not copied or tampered with.

Sunday, November 28, 2021

The reaction of central banks from around the globe on monetary policies during the global finance crisis of 2008.

After the emergency of the new variant of covid named Omicron (as Greek, let's call it o), bringing back up all the climb risk appetite with the greed level of markets dropping. Let's go back to remember an another case of a systemic crisis that bring and escalated to the global financial markets starting as a a mortgage crisis with over-indebtedness targeting buyers of low-income homes, excessive risk-taking by financial institutions and the creation of the United States real estate bubble. The initial approach with monetary policy tools with reductions in stock requirements, ie the required reserve that should be available and maintain the banking system (overnight at the treasuries or at the central bank), discount rate fluctuations charged by central banks to commercial banks as well as in open market operations with the central bank buying securities by adding cash to banks' reserves was found to be unsuccessful. It thus created the need to resort to a monetary policy to address the liquidity trap where it had been created.

The measures taken by the central banks such as (FED, ECB, BOC, BOJ, BOE) were aimed at quantitative easing, increasing the size of their balance sheet, which was mainly done by selling bonds as a rule with the primary goal of changing the overall reserve offer of the economy as they were formed and the amount of money stimulating market liquidity. But also the quality relaxation regarding the change of the structure of the data that the central bank has in its balance sheet as the assets where it held may have an increased risk in the relative price changes that may have an inflationary tendency. And finally with the commitment to provide future guidance to keep short-term interest rates low in order to help meet future monetary policy expectations.

Non-conventional instruments contributed to the easing of monetary policy after the zero interest rate was reached. Most studies find the cumulative effects of quantitative easing and future guidance on long-term government bond yields significant. Negative interest rates have been a very effective tool in reducing bond yields and the short-term yield curve that fell below zero after their implementation. Unconventional monetary policy has helped reduce corporate returns, raise stock prices and devalue the exchange rate.

It is observed that non-conventional monetary policy tools are more effective in times of heightened economic hardship where quantitative easing needs to be stronger and less effective when deflationary pressures increase.

Friday, November 19, 2021

Citi FX weekly outlook

Soaring commodity prices remain a headwind to JPY as Japan remains a large net energy importer and thus higher energy prices tend to lead to lower Japanese terms of trade. But with USDJPY testing levels well above 114.00 recently that now leads to a weaker Yen real effective exchange rate at a level not seen for six years. Citi suggests that this may tempt the BoJ to now allow Yen rates to rise to stabilize alongside US yields to support the Yen somewhat at the current levels. USDJPY manages a sub 114.00 close on Friday with resistance seen at 114.50 -80 while first support comes at 113.25 (range lows) followed by 112.25 (October pivot).

Currently (as of Oct):

• USDJPY: 6 – 12 months: 114.0

• USDJPY: Longer term: 112.0

Previously

• USDJPY: 6 – 12 months: 112.0

• USDJPY: Longer term: 112.0

MT Bias: Turning neutral JPY vs USD & Tactically bearish JPY vs USD, SGD,

AUD, NZD, CAD

Thursday, November 11, 2021

Do we have a "TOP UP"

We had many news corresponding this week. Japan October PPI +1.2% m/m (expected +0.4%), US October CPI +6.2% y/y (vs +5.8% expected), Japan's PM Kishida says wants to compile a further economic stimulus package on November 19. All joining the negative side of dollar but yet the yen collapse. Credit Suisse sold us USD/JPY set to soar as high as 123.00 but as the correlation displays the negative trait of USD with strength loosing over time and per stimulus to be issued of Japan's side, we intimating a bear run. We were right of the bear runs at the past, we did not run for bullish corrections as the main trend seems to have change. The yen is a light weight currency taken buy the strong dollar wind.

Friday, October 29, 2021

Options expire coincidence

We know that DXY can move a lot, in favor or negative with the correlated dollar pairs. Continuing or change the direction of the trend before even gets completed. Alternately boost up the momentum without providing any overbought or oversold, RSI signal even when microeconomic news don't offer any change. There's a big order of USD/JPY options that expires today with strike price at 113.9 dollar. This classic paradigm today with will change trend moving upwards just to close near a big option order at 113.936 above100h morning average and 200h moving average at 113.92 which indicates topping near resistance with a immediate bounce back even when at the right time lands good news boosting USD. Placing an order following the trend providing profits -doesn't mean that you collected the maximum available-.

Descriptive analysis of Yen pair with BTC

The pair of YEN seems to be correlated negative with the rise of Bitcoin. Risky traders prefer to choose on alternative method of investing rather than buying Japan's safe currency. With the scatter plot comparing USD/JPY with Bitcoin linear line has a positive incline with JPY median and mean staying before Bitcoin's. The volatility of cryptocurrency world does not help the standard deviation comparing to Yen of 1.16 having the closing prices near median of 110 which happens to be also the mean.

| Descriptives | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| USD/JPY Close | BTC Close | USD/JPY Low | USD/JPY High | BTC Low | BTC High | ||||||||

| N | 64 | 64 | 64 | 64 | 64 | 64 | |||||||

| Mean | 110 | 45732 | 110 | 111 | 44148 | 46881 | |||||||

| Median | 110 | 46211 | 110 | 110 | 44575 | 47249 | |||||||

| Standard deviation | 1.16 | 6302 | 1.07 | 1.13 | 6075 | 6260 | |||||||

| Minimum | 109 | 29864 | 109 | 109 | 29336 | 31004 | |||||||

| Maximum | 114 | 62496 | 114 | 114 | 56916 | 62719 | |||||||

Monday, October 25, 2021

Banking role

The key role of financial intermediaries and financial markets is to provide a mechanism which resources are transferred and allocated to the most productive opportunities.

No need for intermediation of funds (ie banks):

- Direct financing: borrowers receive funds directly from lenders in the financial markets (with obstacles, difficulty and expense in meeting the needs and their incompatibility)

- Financial claim (any financial asset eg share): a claim for payment of a future total amount of money (or periodic) which implies an obligation for the issuer (borrower) to pay interest periodically and to repurchase the receivable at a fixed value of three (financial) ways:

- On request

- After a specified notification period

- On a specific date or within a time frame

Weekly Citi's Forecast

Citi FX outlook

The fundamental backdrop remains bearish for JPY as – (1) UST yields continue to rise steadily leaving US – Japan rate differentials weighing on JPY; and (2) Japanese investor flows not favoring a stronger Yen – recent monthly data from Japan’s MoF do show Japanese investors turning net buyers of foreign bonds. The team remains bullish JPY vs USD, targeting a rising channel base at 109.11-15.

Previously

- USDJPY: 6 – 12 months: 112.0

- USDJPY: Longer term: 112.0

Currently (as of Oct):

- USDJPY: 6 – 12 months: 114.0

- USDJPY: Longer term: 112.0

MT Bias: Turning more neutral JPY vs USD; Bullish JPY vs EUR, CHF

Tactically modestly bearish JPY vs USD

Tactically bearish JPY vs Commodity FX (AUD, NZD & CAD), GBP and Asia EMFX (CNH & SGD)

Friday, October 22, 2021

Sealed case

It's the final day of the week and the yen settles downwards. Friday today had a welcome surprise with rising CPI helping Japan to rise closer to near 2% inflation aiming. The Bank of Japan monetary policy meeting is on October 27 & 28 will held new Information and There have been rumours of expected forecast downgrades to be included in the new outlook which probably will help the rise of yen pairs. As for Technical analysis we are near a gorge, a move forward means the downfall of USD/JPY bringing back the old resistance of 109-110 level. Zone than occupied more than 10 weeks in the past going side ways.

|

| 1h chart of USD/JPY |

Thursday, October 21, 2021

OIL Drowdown

The rise of JPY happened as a contribution from the knock over of commodities. Japan, a heavily industrial country importing mainly energy and Special oil from Asian cartel. OPEC today node negative to a lower oil price coming from increasing output to supply the demanding zone of G3. Strange the oil follows the firm dollar and the weak loonie after weeks of top currency. The only Strong of the day seems to be the Yen, safe choice over volatility times.

On point

USD bulls went to stocks. The currency today dive DXY 93.5, same story with bitcoin

as 66.5k triggered the down alarm to lose 2.5k from the start of the day. JPY rose as forecasted without any news correlated today. The big highlight of the day was US initial jobless claims 290K versus 300K estimate, a nice welcome drop to unemployment but somehow did not triggered right away the rise of dollar leaving it down 0.02%. Two pictures of correct forecast of the week.

Tuesday, October 19, 2021

Short USD/JPY

USD seems to be losing strength as well as yen, but the momentum of yen currency push the pair downward. We have multiple tries with dollar fail rally attempts, with bulls keep inconsistent push while short side keep strengthen. Unfortunately today was a quiet day without any economic calendar news thous is possible to see a closing near to open Price. Tomorrow is a totally different thing, I see a rapid downfall of USD/JPY possible to close near 113.5 but this is just a guessing while we have many important news coming tomorrow as can be collaborated with both currencies up and down.

|

| USD/JPY 1D |

Wednesday, October 13, 2021

FOMC aftermath

FOMC minutes results: Reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS)

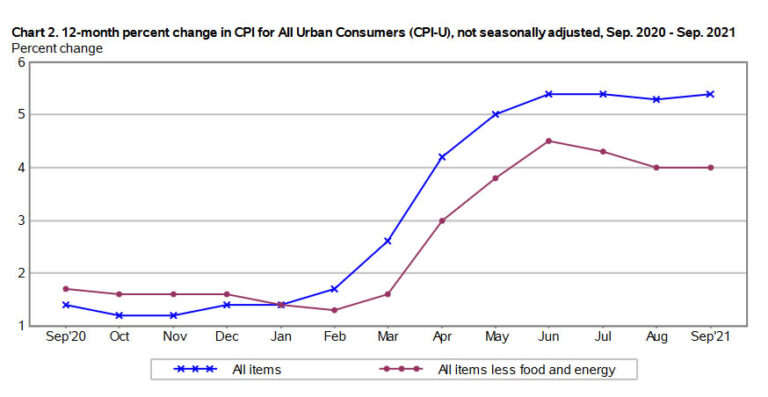

CPI outcome: Core Inflation Rate YoY unchanged 4% and Inflation Rate YoY 5.4% +0.1% more than expected.

Dollar index retreated to 94.1 with fear of inflationary pressures remained high in September helping the equities to rally US500 +0.28% USNDX+0.76%. FOMC showed that it is close to start tapering, possibly in mid-November with hike rates possible at late 2022 or early 2023.

As predicted, JPY rallied USDJPY: 113.28 -0.27 -0.24%

|

| CPI DATA |

|

| Dollar index DXY |

JPY rally

This is the first day seeing a JPY rally after from a row of 13 red days. Japanese equities tried the mega squeeze in September, but that is gone.

"Japanese equities have done nothing since February. The recent excitement was all about the reflation trade happening, but despite the surge in yields, TOPIX has refused bouncing much. The only difference this time around is the fact people have bought into the story..." - themarketear

Moving on, there's CPI report coming 12:00 pm GMT with inflation waiting to be 5.3% and the core one 4%. Today we shall approach using Buy the rumor Sell the news method. This ancient strategy provides not only risk free action but also the power of jumping early at the profits wagon. Getting serious, just avoid placing any orders during pre. news as volatility is low during that hours. The safe bet today is 113.0 - 113.5 for USD/JPY being the zone of expiring options.

Tuesday, October 12, 2021

Weekly Citi's Forecast

Citi FX outlook

The fundamental backdrop remains bearish for JPY as – (1) UST yields continue to rise steadily leaving US – Japan rate differentials weighing on JPY; and (2) Japanese investor flows not favoring a stronger Yen – recent monthly data from Japan’s MoF do show Japanese investors turning net buyers of foreign bonds. The team remains bullish JPY vs USD, targeting a rising channel base at 109.11-15.

Previously

- USDJPY: 6 – 12 months: 112.0

- USDJPY: Longer term: 112.0

Currently (as of Oct):

- USDJPY: 6 – 12 months: 114.0

- USDJPY: Longer term: 112.0

MT Bias: Moderate bearish JPY vs USD;

Modestly bullish JPY vs EUR

Tactically moderately bearish JPY vs USD;

Tactically bearish JPY vs Commodity FX (AUD, NZD & CAD), GBP and Asia EMFX (CNH & SGD)

Sell signal

Yes, I do get a TDI sell signal as Bollinger bands contract waiting for a burst move downwards. Now 09:00 am GMT, both London and European markets open. The move to place a short trade today is risky, I counter offer you to wait for CPI tomorrow Wednesday. The USD/JPY seems to have been settle to 113.5 area. A move up will break towards to 114.17 - 114.5 price zone. The move upwards is limited in compare of the downside which can easy drop to 110.0 who was a immersive support zone. Tomorrow is the big market day.

The price fluctuates as the longs rose 7.3% today but consumer sentiment favors the short side at the moment with weekly longs dropped by 10.19% according to IG. Fear and energy crisis plays a huge role coming from Evergrande crash delaying the third bond payment.

|

| Price density areas-Price data-Bollinger bands density-Sentiment |

USD/JPY correlated to commodities

The raise of commodities does not justify the weakening of JPY. As the rapid raise of energy markets occur so does the treasury yields and strength of DXY index happens. The up rise of Yen seems to be more correlated to USD rather than commodities. Bellow the USD/JPY pair next to coal and WTI oil. Japan's substantial reliance on imports for fuel, raw materials, and food, domestic industries are equally exposed to higher prices from a weak yen. This is why Japan favors for a strong currency.

|

| WTI, Coal & USDJPY from Sep 1, 2021 till Oct 12, 2021 |

A different approach today

We explore the correlation of JPY with the other currencies. As we expect JPY is heavily dependent in coal and oil making it to responds negatively to heavy commodities pairs AUD,CAD and NZD.

Bellow the two charts, the one with correlations and the other with currency market moves. Do we approach to the AUD & CAD overheat that needs a cooldown? Which currencies do depend more to se a opposite move from them taking the lead afterwards.

|

| Correlation |

|

| Market glance |

Monday, October 11, 2021

USD/JPY trinity

Adding more to USD/JPY weekly stats of DXY/US10YT/USDJPY since 2016 till Oct 2021 here is the graph with DXY/US10YT/USDJPY. As we can see the price correlates better with treasury yields rather than DXY dollar index. Same happens with US10YT and DXY.

|

| USD/JPY with US10YT and DXY |

1H currency strength index

As forecasted, bull momentum skyrocketed USD/JPY in Asian/early Europe session. The close will be near open or higher? The retrace to 50% waits for Wednesday's CPI or Friday's retail sales.

Todays support and resistance seems to have been form.

Resistance: 113.863 - 112.064 - 111.694 - 110.465

Support: 109.187 - 108.496 - 107.617 - 104.732

Resistance: 113.863 - 112.064 - 111.694 - 110.465

Support: 109.187 - 108.496 - 107.617 - 104.732

Sunday, October 10, 2021

Start of the week with USD/JPY point of view

Its before 8am in New Zealand, and as is usual for a Monday morning, market liquidity is light. Some small change from late Friday levels with USD/JPY dropping slightly to 112.14

Pair rose as the bullish push from nonfarm payrolls was massive. The data did not cope (expecting higher stats) and the funds didn't dump treasury yields with S&P closing lower pushing all along the USD currency.

Asian and Europe session expects to have the most volatility and volume today as US Columbus day and Thanksgiving for CAD will drop the liquidity later on. We expecting a correction to 23.6% 111.475 or 38.2% today 111.000 but the first move of the day will push the price a little higher as bullish momentum of Friday kept the currency idea upwards. The close will be near open price or somewhat lower.

USD/JPY weekly stats of DXY/US10YT/USDJPY since 2016 till Oct 2021

The tables of Descriptive analysis and correlation of US dollar index, 10 year treasury yields and USD/JPY weekly close data.

Descriptives

| Descriptives | |||||||

|---|---|---|---|---|---|---|---|

| DXY | Price | DGS10 | |||||

| N | 301 | 301 | 301 | ||||

| Missing | 0 | 0 | 0 | ||||

| Mean | 95.5 | 109 | 1.94 | ||||

| Median | 95.7 | 110 | 1.91 | ||||

| Standard deviation | 3.17 | 3.47 | 0.707 | ||||

| Minimum | 89.1 | 100 | 0.550 | ||||

| Maximum | 103 | 121 | 3.21 | ||||

Correlation Matrix

| Correlation Matrix | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| DXY | Price | DGS10 | |||||||

| DXY | Pearson's r | — | |||||||

| p-value | — | ||||||||

| Price | Pearson's r | 0.344 | — | ||||||

| p-value | < .001 | — | |||||||

| DGS10 | Pearson's r | 0.084 | 0.536 | — | |||||

| p-value | 0.147 | < .001 | — | ||||||

Bonus: correlation plot with density graph

Friday, October 8, 2021

10-year Treasury yields importance today

10-year yields adds another 2 bps today to 1.59% and close to cross the 1.60% mark a technical area of last month breakout. My point of view is that bond sellers will go after profit taking, distribution and a mark-down activity. All that depends a lot on what the US nonfarm payrolls release will be later today.

Scatterplot of US10Y 2016 weekly till today correlated with weekly's close price:

Wednesday, October 6, 2021

JPY Citi views & strategy Bias/ Forecasts/ Key level

Citi FX outlook

The latest BoJ Tankan report reveals the USDJPY breakeven target for Japanese manufacturers at 107.64 in FY2021 which is a considerable distance from current levels around 111.00 and which means little need for Japanese exporters to sell USD to hedge their export earnings at current levels.

Previously

• USDJPY: 6 – 12 months: 112.0

• USDJPY: Longer term: 112.0

• USDJPY: 6 – 12 months: 112.0

• USDJPY: Longer term: 112.0

Currently (as of Sep):

• USDJPY: 6 – 12 months: 112.0

• USDJPY: Longer term: 112.0

• USDJPY: 6 – 12 months: 112.0

• USDJPY: Longer term: 112.0

MT Bias: Moderately bearish JPY vs USD;

Neutral JPY vs EUR; Short CAD vs JPY

Tactically bearish JPY vs USD,

Commodity FX (AUD, NZD & CAD),

GBP and Asia EMFX (CNH & SGD)

Tuesday, October 5, 2021

Stock market today taught us

Every stock market price depends on:

- projected earnings per share

- period of realization of profits

- projected profit risk

- use of loan funds

- company dividend policy

The objective of a company is to maximize the wealth of the shares and not to maximize profits (microeconomic approach) as the risk of returns and the timing of the implementation of investment programs are not taken into account.

Main project of every company follows these three Financial principles:

- Investment decision: finding, evaluating and selecting investment programs where they will be carried out in the future in risky conditions with the possibility of being different from the expected returns. This is how we set minimum efficiency penalties. The CFO* also makes decisions about the assets as well as to modify and replace them.

- Financing decision: Excellent capital structure where it maximizes the common share price or minimizes the total capital cost. It affects current and future investment program activities by setting a minimum required return.

- Dividend policy: decision to distribute profits as dividend or withholding for investment in investment programs (degree of internal financing). It affects the stock market price and is associated with the excellent capital structure.

*CFO: responsible for raising funds and using them to increase corporate value.

Subscribe to:

Comments (Atom)

Popular Posts:

-

Value investing is a tried-and-tested strategy that focuses on identifying stocks trading below their intrinsic value. One powerful tool for...

Value investing is a tried-and-tested strategy that focuses on identifying stocks trading below their intrinsic value. One powerful tool for... -

Strategic Framework Recap The preceding three-part series established a complete quantitative trading workflow beginning with market data ...

-

Introduction to Systematic Strategy Development The development of robust quantitative trading strategies requires a systematic approach t...